Why Banks Freeze Crypto Accounts in 2026: A Guide to Avoiding Lockouts

May, 18 2026

You deposit your hard-earned cryptocurrency into your bank account, only to find it locked. No warning. No explanation. Just a message saying your funds are under review. If this sounds familiar, you are not alone. In 2026, bank account freezing for crypto activity has become the standard operating procedure for traditional financial institutions dealing with digital assets. It is no longer just about illicit actors; everyday users, merchants, and even small businesses face sudden restrictions simply because their transaction history intersects with high-risk blockchain addresses.

This shift isn't accidental. It is the direct result of a regulatory overhaul that accelerated dramatically in 2025. With the passage of the GENIUS Act and updated guidance from the Federal Deposit Insurance Corporation (FDIC), banks now have both the legal authority and the technical tools to freeze accounts preemptively. The goal? To stop money laundering and terrorism financing before it happens. The side effect? Legitimate users getting caught in the crossfire of overly aggressive automated compliance systems.

The Regulatory Shift: From Warning to Action

To understand why your account might get frozen today, you need to look at what changed yesterday. For years, banks operated under vague guidelines that discouraged crypto involvement but didn't explicitly ban it. That ambiguity ended in mid-2025. The Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act became law, creating the first comprehensive federal framework for digital assets in the United States.

GENIUS Act is a federal legislation signed into law in June 2025 that establishes regulatory standards for stablecoins and defines enforcement mechanisms for freezing crypto-related assets. This law gave regulators a clear definition of a "lawful order," allowing them to issue writs that require banks to seize, freeze, or prevent the transfer of payment stablecoins. Unlike previous regulations that focused on exchanges, this act extends enforcement directly to traditional banks.

Simultaneously, the FDIC rescinded its restrictive guidance FIL-16-2022 in April 2025. While this might sound like good news for banks wanting to offer crypto services, it came with a catch. Institutions could engage in crypto activities without prior approval, but only if they maintained "adequate risk management practices." In practice, this meant banks had to build robust Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT) controls. Since building these controls takes time and money, many banks chose the safer route: freeze any suspicious activity until they can verify it manually.

How Blockchain Analysis Triggers Freezes

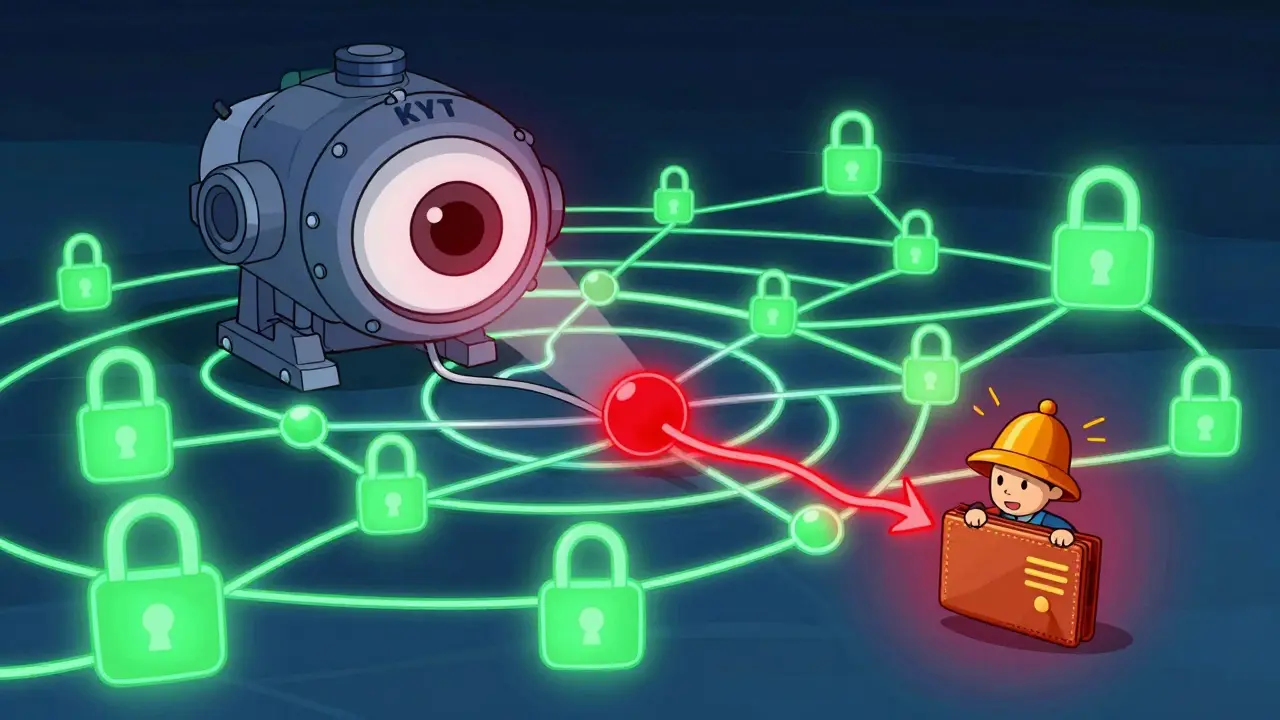

You might think, "I bought Bitcoin legally. Why would my bank care?" The problem is that blockchain is transparent. Every transaction is recorded publicly, linking addresses together in a complex web. Banks don't just look at your immediate transaction. They use sophisticated Know Your Transaction (KYT) monitoring systems to trace the history of the coins you received.

If the cryptocurrency you deposited passed through an address associated with darknet markets, sanctioned entities, or mixing services-even once-your bank's algorithm flags it as high-risk. You don't need to have done anything wrong. You just need to have received funds from someone who did. This is known as "indirect exposure."

Consider this scenario: You sell freelance services and accept USDT (Tether) as payment. Your client paid you using coins they received from a peer-to-peer platform where another user had previously interacted with a sanctioned wallet. Your bank's KYT system sees that connection. Within minutes, your account is restricted. The burden of proof shifts entirely to you to demonstrate that your source of funds is clean, regardless of whether you knew about the upstream illicit activity.

| Trigger Type | Description | Risk Level |

|---|---|---|

| Direct Illicit Link | Funds sent directly from a known criminal address | Critical |

| Mixing Service Exposure | Funds passed through a privacy-enhancing mixer | High |

| Sanctioned Entity Interaction | Indirect link to OFAC-sanctioned wallets | High |

| High-Frequency Trading | Rapid movement of large sums across multiple accounts | Medium |

| Unverified Source | Lack of documentation for large deposits | Medium |

The Off-Ramp Bottleneck

The most common point of failure is off-ramping-converting cryptocurrency back into fiat currency like USD or NZD. Banks view this step as the final gateway where illicit funds enter the traditional economy. As a result, they scrutinize every withdrawal request.

In 2026, major banks increasingly require extensive documentation before crediting accounts or allowing withdrawals. This includes proof of purchase, tax records, and sometimes even affidavits explaining the purpose of the transaction. For individual users, gathering this paperwork can take weeks. During this time, your funds are inaccessible. For businesses relying on cash flow, this delay can be catastrophic.

Neobanks and fintech apps, which initially welcomed crypto users, have also tightened their policies. Platforms like Cash App, PayPal, and Wise now enforce stricter KYC (Know Your Customer) checks. If your behavior deviates from normal patterns-such as suddenly receiving large amounts of crypto-they may freeze your account pending investigation. This creates a bifurcated market: large institutions gain regulatory clarity and start offering stablecoin services, while individual users face increased scrutiny and barriers.

What You Can Do to Protect Yourself

You cannot control the entire blockchain history, but you can manage your risk. Here are practical steps to minimize the chance of an account freeze:

- Use Clean Sources: Only receive funds from reputable exchanges or trusted individuals. Avoid peer-to-peer platforms unless you fully trust the counterparty.

- Document Everything: Keep detailed records of all crypto transactions, including invoices, receipts, and communication logs. If your bank asks for proof, you should be able to provide it immediately.

- Avoid Mixing Services: Never use tumblers or mixers to obscure your transaction history. These are red flags for compliance algorithms.

- Spread Out Transactions: Instead of moving large sums all at once, break them into smaller, regular transfers. This looks less like layering-a technique used in money laundering.

- Communicate Proactively: If you plan to make significant crypto deposits, inform your bank in advance. Some institutions allow pre-approval for known activities.

Additionally, consider diversifying your banking relationships. Don't keep all your crypto-related funds in one account. Use separate accounts for personal expenses and business transactions. This limits the damage if one account gets frozen.

The Future of Crypto Banking

The regulatory landscape continues to evolve. The GENIUS Act was just the beginning. Other legislation, such as the Digital Asset Market Clarity Act (CLARITY Act), passed by the House in July 2025, aims to further define the boundaries between securities and commodities. Meanwhile, the CBDC Anti-Surveillance State Act reflects growing concerns about government oversight of digital payments.

For now, the trend is clear: banks will continue to prioritize compliance over convenience. The cost of failing an audit far outweighs the inconvenience of freezing a customer's account. As a result, we may see more users turning to decentralized finance (DeFi) platforms that operate outside traditional banking infrastructure. However, DeFi comes with its own risks, including smart contract vulnerabilities and lack of consumer protection.

Until regulators strike a balance between innovation and security, bank account freezing for crypto activity will remain a persistent challenge. By understanding the rules and taking proactive steps, you can navigate this new reality with greater confidence.

Why did my bank freeze my account after a crypto deposit?

Your bank likely detected a link between your deposit and a high-risk blockchain address. This could include interactions with darknet markets, mixing services, or sanctioned entities. Even if you acted legally, indirect exposure can trigger automated freezes.

How long does it take to unfreeze a crypto-related account?

Resolution times vary widely. Simple cases may resolve in days if you provide complete documentation. Complex investigations involving multiple transactions can take weeks or even months. Contact your bank immediately to expedite the process.

Is it illegal to receive crypto from a questionable source?

Not necessarily. Receiving funds unknowingly from a tainted source is not always illegal, but it can lead to civil penalties or account closures. Criminal charges usually require intent or negligence in verifying the source of funds.

What is the GENIUS Act and how does it affect me?

The GENIUS Act is a 2025 U.S. law regulating stablecoins. It gives banks clearer authority to freeze crypto assets linked to illicit activities. For users, this means stricter scrutiny of transactions and faster enforcement actions.

Can I avoid account freezes by using DeFi instead?

Decentralized finance platforms do not rely on traditional banks, so they are less likely to freeze your assets. However, DeFi carries other risks, such as smart contract bugs and lack of recourse if something goes wrong. Additionally, converting DeFi assets to fiat still requires a regulated exchange or bank.